Middle East Automotive Glass Tinting and UV Protection Market Outlook 2024-2030

Executive Summary

The Middle East's automotive glass tinting market is driven by extreme heat and strict tint regulation. UV-protection awareness, luxury vehicle growth, and ceramic-film innovation are pushing the market from USD 1.2 Billion in 2024 toward roughly USD 1.6 Billion by 2030, with solar-control films leading demand.

Key Market Velocity Data

- Current Market Value: USD 1.2 Billion in 2024

- Projected Market Value: around USD 1.6 Billion by 2030

- CAGR: about 5% during 2025 to 2030

- Most Popular Type: solar control films, ahead of privacy and ceramic

- Primary Growth Catalyst: extreme heat, UV awareness, and aftermarket demand

What Is Driving Demand in the Middle East Tinting Market?

Demand is climate and comfort led. About 60% of vehicle owners now prioritize UV protection, and regional luxury vehicle sales are projected near 1.5 million units, lifting premium film demand. Extreme Gulf heat makes solar-control and ceramic films near-essential, while ceramic products deliver infrared rejection of up to 96% to 98%. Year-round sun exposure makes heat and UV rejection a constant purchase, not a seasonal one, and tinting is now standard at the point of vehicle purchase.

- UV awareness: about 60% of owners prioritize UV protection in film selection.

- Luxury demand: regional luxury sales near 1.5 million units lift premium film attach rates.

- Heat performance: ceramic films reject up to 96% to 98% of infrared heat.

- Aftermarket strength: extreme heat and customization keep aftermarket demand robust.

How Do Tint Regulations Shape the Market?

Regulation defines product specs. In the UAE, the Roads and Transport Authority allows side and rear tint to 50% VLT and front side windows to 30%, with windshields kept at 70% minimum light transmission, and a fine of AED 1,500 for violations (Dubai RTA). A 2023 UV-compliance standard reinforced the rules. Approved film lists are tightening what installers can legally fit.

Saudi rules are stricter on front glass. Side, rear, and front windows must keep at least 30% transparency, front side windows cannot be tinted, and two-door cars and taxis are barred from tint, with fines of 500 to 900 SAR. These standards push demand toward compliant, high-clarity ceramic films. Compliance checks at registration renewal steer owners toward certified products.

Which Companies Are Shaping the Competitive Landscape?

Global film majors lead the premium tier. 3M blocks up to 99% of UV rays with its Crystalline line, XPEL's XR Plus delivers up to 98% infrared rejection, and Llumar, owned by Eastman, distributes across more than 100 countries. SunTek's CeramicIR reaches up to 96% infrared rejection. Lifetime warranties are becoming a key differentiator at the premium end.

Specialists and value brands fill the rest. Hanita Coatings markets its SolarZone solar-control films, while Solar Gard, Madico, Huper Optik, Avery Dennison, and Johnson Window Films compete across price tiers. Differentiation runs on infrared rejection, clarity, and warranty rather than price alone. Local distributors and certified installer networks decide regional reach.

What Does This Mean for B2B Decision-Makers?

For film makers, installers, and investors, the market is premiumizing toward ceramic and compliance-grade films, and performance now decides margin. With the market moving from USD 1.2 Billion toward roughly USD 1.6 Billion by 2030 at about 5% CAGR, growth is steady, but regulation and heat performance define winners. Brand authentication is rising as counterfeit films pressure margins.

- For film makers: prioritize ceramic lines, where infrared rejection reaches up to 98%.

- For installers: guarantee compliance with UAE's 50% and Saudi's 30% VLT limits.

- For investors: back Saudi Arabia, projected as the fastest-growing regional market.

- For dealers: bundle premium film with luxury sales near 1.5 million units.

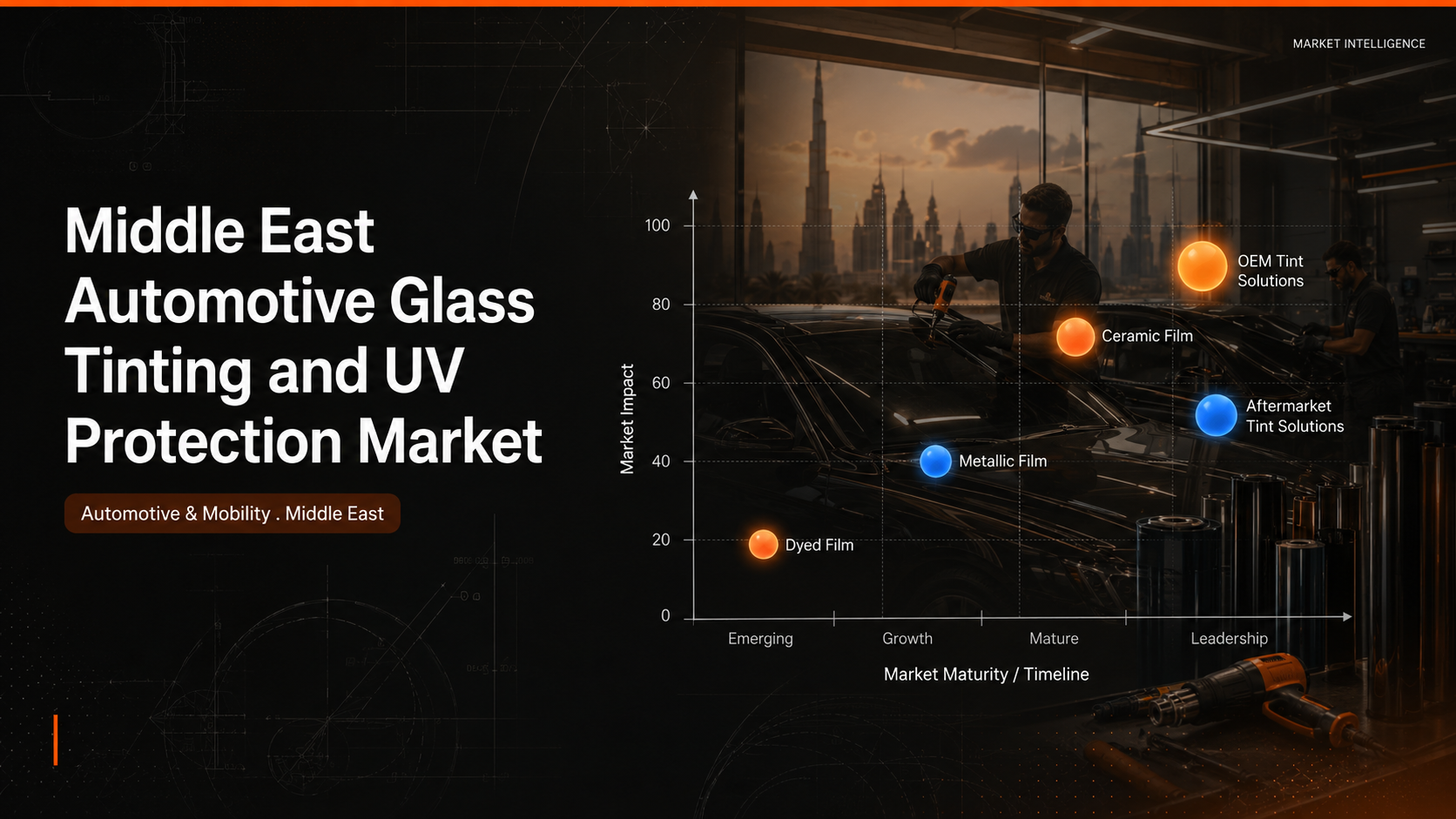

Which Segments and Channels Lead the Middle East Tinting Market?

Segment economics favor solar-control and ceramic films through the aftermarket. Solar-control films lead volume, ceramic films grow fastest on heat performance, and privacy and safety films serve niches. Individual vehicle owners dominate demand, while dealerships and fleet operators scale OEM and bulk installation. Paint protection film is an adjacent, fast-growing premium category, while decorative wraps add a customization-led revenue stream.

- Film mix: solar-control films lead, while ceramic grows fastest on infrared performance.

- Application: windshield film is the fastest-growing application segment.

- Channel: aftermarket leads, with dealerships and fleets expanding OEM-grade installs.

Ken Research Strategic Outlook

The decisive lever in Middle East tinting is regulation plus heat performance, not price. As VLT enforcement tightens and ceramic technology improves, margin will migrate toward brands that pair high infrared rejection with compliance-grade clarity. Expect Saudi Arabia to lead regional growth and ceramic films to take share from dyed and metallic, pushing the market toward USD 1.6 Billion by 2030. Counterfeit crackdowns will favor authenticated, warrantied brands.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Middle East Automotive Glass Tinting and UV Protection Market Report

Comments

Post a Comment