Vietnam Commercial Drone Market Outlook 2024-2030: Growth Drivers and Forecast

Executive Summary

Vietnam's commercial drone market reached USD 65 million in 2024, and the binding constraint is not demand. It is defence-controlled licensing, with only 300 operators approved even as precision agriculture and infrastructure inspection pull demand higher.

Key Market Velocity Data

- Current Market Value: USD 65 million in 2024

- Projected Market Value: approximately USD 135 million by 2030

- CAGR: about 13% during 2025 to 2030

- Dominant Segment: rotary-wing drones, agriculture and inspection-led

- Primary Growth Catalyst: precision agriculture, infrastructure inspection, and regulatory opening

What Is Driving the Market?

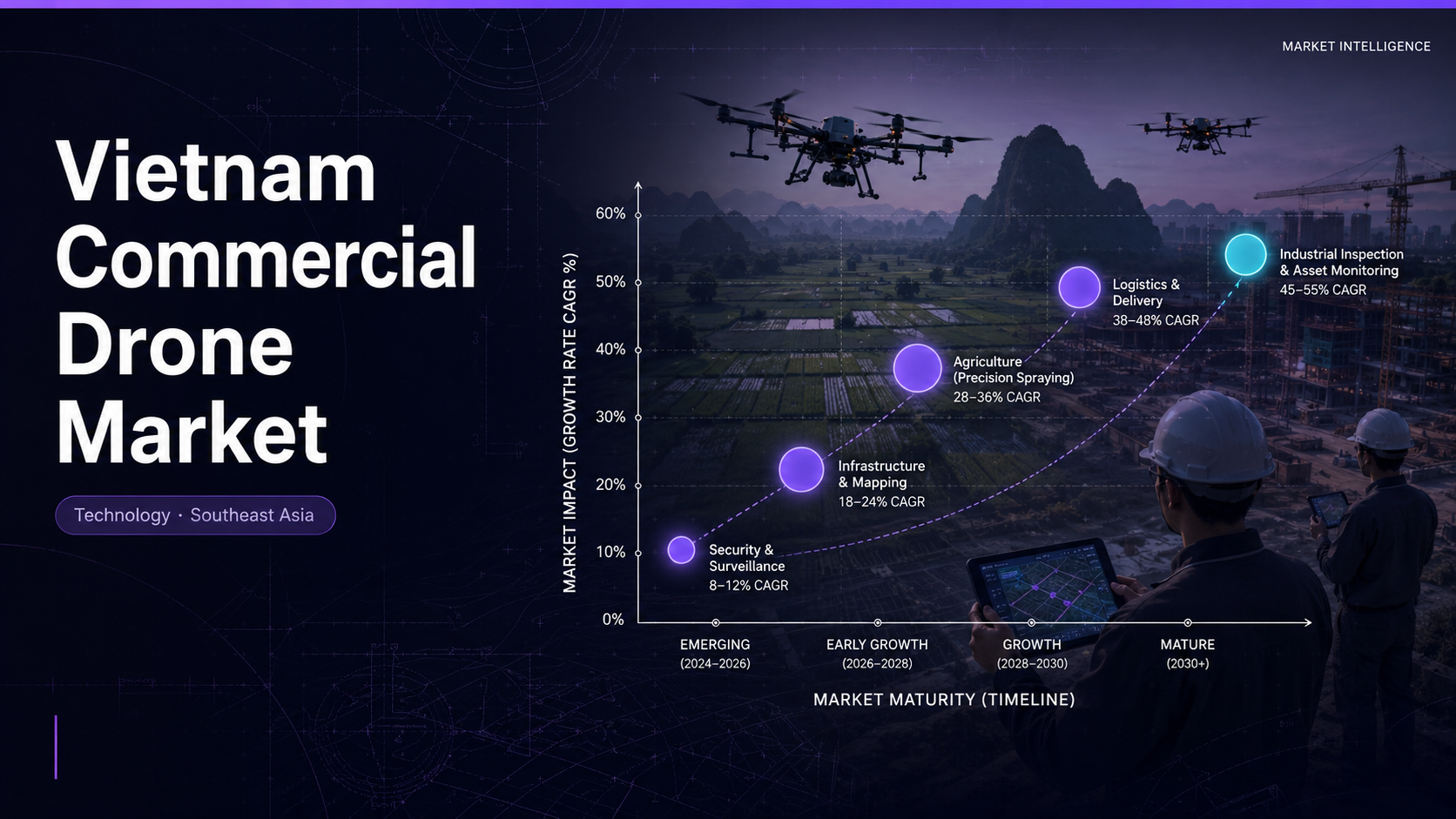

Agriculture and inspection lead demand. Precision spraying, crop monitoring, and infrastructure surveys are the primary use cases, and the market sits at USD 65 million in 2024, projected toward USD 135 million by 2030 at about 13% CAGR. Agricultural drones alone represent roughly 800 units of demand. Vietnam's vast rice and coffee farming base makes aerial spraying a natural efficiency play.

Technology and policy are converging. Drones now offer 30-plus minute flight times and 5kg payloads, while the 2024 Law on People's Air Defence formalized UAV definitions. Agriculture flights get 180-day permits versus 30 days for general use, a deliberate tilt toward farming. This regulatory clarity is starting to convert informal usage into licensed commercial operations.

- Agriculture: crop-spraying and monitoring drive demand, with roughly 800 agricultural units

- Surveillance: aerial inspection demand is projected near 1,200 units across infrastructure and security

- Technology: 30-plus minute flight times and 5kg payloads expand commercial use cases

- Policy tilt: agriculture flights receive 180-day permits, far longer than the 30-day general limit

Which Entities Are Shaping the Market?

Global hardware dominates supply. DJI leads, with Parrot, Yuneec, senseFly, Skydio, AeroVironment, and Delair competing across fixed-wing, rotary, and hybrid platforms. Local players Flycam Pro and RT Robotics provide services and integration across the USD 65 million market, where only 300 operators are licensed. Most demand is met by imported hardware, with local firms competing on service, training, and data analytics.

Platform mix is clear. Rotary-wing leads by type, suited to spraying and inspection, while fixed-wing serves mapping and nano or micro drones handle close-range tasks. Agriculture and construction are the largest end-users, ahead of logistics, public safety, and energy across a market growing at about 13% CAGR. Data and software, not just airframes, increasingly determine which operators win contracts.

The Ministry of National Defence controls the airspace. Circular 19/2019 governs operations, and the 2024 Law on People's Air Defence added formal UAV definitions, no-fly zones, and permit rules. With only 300 operators licensed, regulation, not demand, is the growth gate.

How Do Segments and Uses Split?

Types and uses concentrate demand. Rotary-wing leads, fixed-wing serves mapping, and hybrid and nano drones fill niches. Agriculture and infrastructure inspection are the dominant applications across the USD 65 million market in 2024, with logistics delivery an emerging frontier. Logistics and last-mile delivery remain pilot-stage but could open a large new segment by 2030.

- By type: rotary-wing leads for spraying and inspection, fixed-wing for mapping

- By use: agriculture and infrastructure inspection dominate, while logistics is emerging

- By payload: 5kg-class drones with 30-plus minute endurance unlock commercial tasks

- By region: agricultural provinces drive spraying demand, while cities drive inspection

What Does This Mean for B2B Decision-Makers?

Win the licensing game first. The USD 65 million market grows about 13%, but with only 300 licensed operators, regulatory access is the real moat. Service providers that secure permits and 180-day agriculture clearances will capture the spraying and survey demand. Permit backlogs and airspace approvals are the practical barrier to scaling fleets quickly.

Local presence and compliance matter more than hardware. The 2024 Air Defence Law and Ministry of Defence permits favor operators who navigate no-fly zones and registration. Hanoi's 11 billion VND crop-spraying trial signals public funding for agricultural drone adoption. Public-sector contracts in agriculture and surveying offer the most reliable early revenue.

- For drone-service firms: secure Ministry of Defence permits and 180-day agriculture clearances early to lock first-mover share

- For agritech players: target precision spraying where public trials and subsidies are emerging across rice and coffee regions

- For investors: back licensed operators, since the 300-operator cap limits competition and protects margins

- For hardware vendors: localize support for DJI-class rotary platforms in farming provinces to win recurring service revenue

Ken Research Strategic Outlook

Ken Research sees Vietnam's commercial drone market as a regulation-gated growth story. The next phase depends on how fast the 2024 Air Defence Law and agriculture-friendly permits expand the licensed operator base beyond 300. Expect the USD 65 million market to roughly double toward USD 135 million by 2030 as precision agriculture and infrastructure inspection scale and the licensed operator base widens.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Vietnam Commercial Drone Market Report

Comments

Post a Comment